Introduction

Blockchain technology is a digital ledger that records, verifies, and keeps track of transactions in a secure and transparent way. It is the underlying foundation for cryptocurrencies like Bitcoin and Ethereum. The blockchain stores every transaction ever made on its network, which makes it difficult to change or reverse any single transaction without also changing all subsequent transactions made by that user’s peers in the network. The blockchain can be used for many other applications beyond cryptocurrencies by enabling users to build trust through consensus algorithms.

Blockchain is a digital ledger

Blockchain is a digital ledger of transactions. It’s a distributed database that keeps track of who owns what, and it allows for secure transactions between parties. In other words, blockchain technology can be used to digitize just about anything that needs to be tracked or stored in an immutable way–from money and valuable assets like real estate or jewelry (which we’ll get into later) all the way down to medical records and birth certificates.

Blockchain has been called many things: “the most disruptive technology since the internet”; “a new type of internet”; even “the future.” But before we dive into those definitions more deeply let’s first make sure we have our terms straight so that we’re all on the same page here!

Blockchain technology has many applications

Blockchain technology is a revolutionary way of storing and verifying data. It can be used to store anything from financial transactions and legal documents, to medical records and academic credentials. Blockchain technology also makes it possible to create new cryptocurrencies (e.g., bitcoin) that are not controlled by any central authority.

Another application for blockchain technology is creating smart contracts: digital agreements between two parties that are executed automatically when certain conditions are met (e.g., when a shipment arrives).

Blockchain works because of encryption

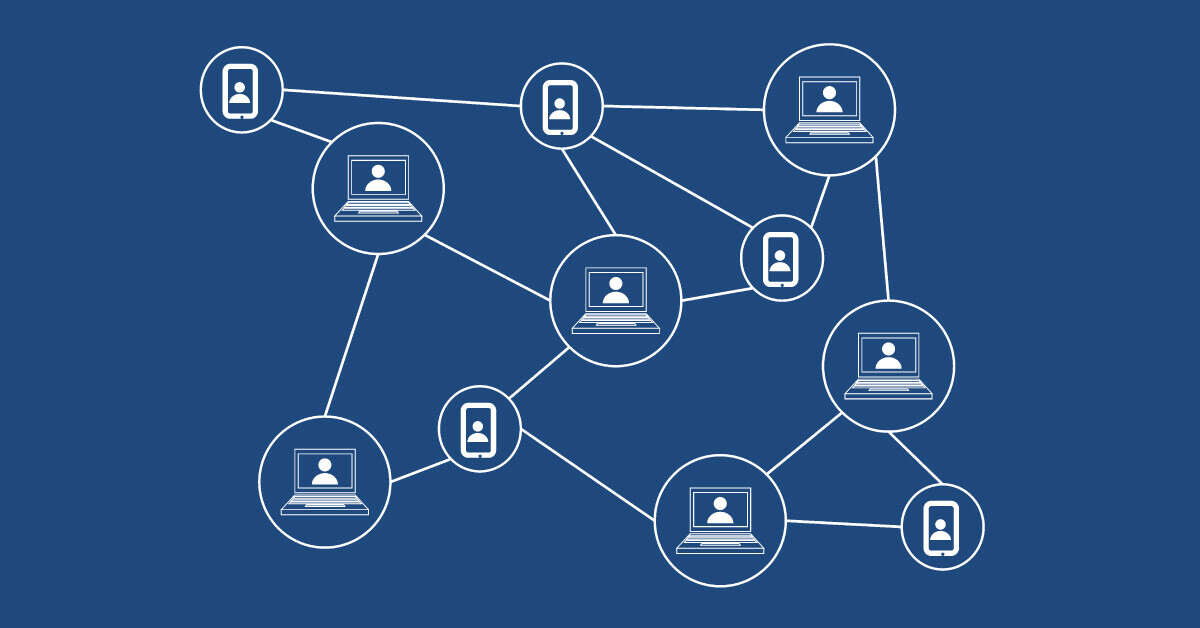

Blockchain works because of encryption. The blockchain is a distributed database that maintains a continuously growing list of records called blocks. Each block contains transactional data and a timestamp, as well as the hash of the previous block in the chain. A hash function takes an input value and creates an output value which is dependent on the input but hard to predict beforehand. In this way, each block’s hash acts like a unique digital fingerprint; if someone tries to modify or tamper with any part of that block’s contents (such as by changing its timestamp), all subsequent hashes will be invalidated because they were computed using this particular data set. This makes tampering with any part of the ledger virtually impossible because doing so would require recalculating all subsequent hashes for every single transaction ever made since its inception – something that would require immense computing power and time even for today’s most powerful computers!

In addition to being immutable, another key feature underpinning blockchain technology is decentralization: instead having one central authority controlling everything from start-to-finish like traditional financial institutions do today (think banks), each member within this peer-to-peer network has equal say over who gets access privileges based upon how much computing power they contribute towards solving complex math problems needed during validation processes like making payments between accounts belonging two different parties involved in transactions involving Bitcoin tokens being sent back forth across thousands scattered around different locations worldwide.”

The blockchain is a distributed database that can be used to verify transactions.

The blockchain is a distributed database that can be used to verify transactions. In other words, the blockchain is a digital ledger where data is stored in blocks and linked together through cryptography.

The idea behind the technology was to create an open, decentralized platform for recording transactions without the need for middlemen or third parties like banks or governments. Blockchain technology enables people who do not know each other and live in different countries/continents/time zones to make transactions with each other securely and efficiently without needing any central authority (e.g., government) involved in those transactions at all!

Blockchain technology has many applications beyond cryptocurrency such as managing supply chain logistics; healthcare records management; voting systems etc…

Conclusion

In the end, blockchain technology is nothing more than a digital ledger. It’s an online database that stores information about transactions and creates an unforgeable record of those transactions. The blockchain was first introduced in 2008 as part of a project called Bitcoin, which aims to create a peer-to-peer electronic cash system that allows people across the globe to send money without going through banks or other intermediaries like credit card companies.