Introduction

Blockchain technology is becoming a hot topic in the world of business. People are talking about it, but they don’t always understand what it really is or how it works. This brief introduction to blockchain technology will answer some common questions and give you the basics.

How does blockchain technology work?

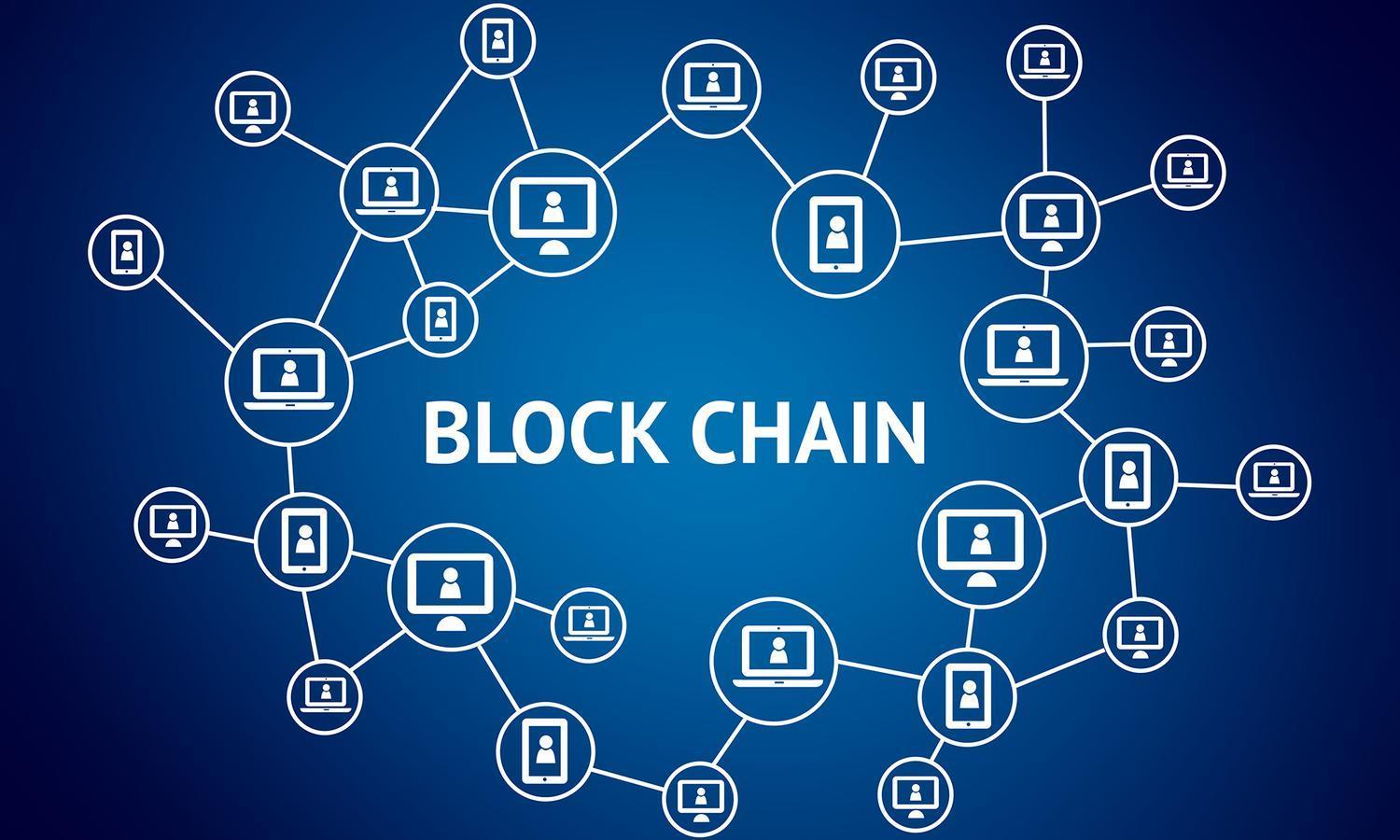

The blockchain is a distributed ledger, or database, that allows for the creation and maintenance of a shared record. Blockchain technology is a transparent, immutable and secure way to store data.

Blockchain technology can be used for many different things–from currency transactions to the recording of land titles, from healthcare records management to identity management systems like passports or driver licenses–and its potential applications are only beginning to be explored by industry and governments around the world.

What is a block?

A block is a group of transactions, and it’s the most basic building block of the blockchain. Blocks are chained together in linear, chronological order using cryptography. A new block can only be added to the chain if it’s accepted by all nodes in the network; this means that no one person or entity can alter or invalidate existing records.

Each block contains the hash (a unique identifier) of its predecessor, along with a timestamp and information about who created it (i.e., which miner). The hash acts like an electronic fingerprint–it lets you verify that you’re looking at an actual transaction on the blockchain rather than some false data being inserted by someone trying to scam or hack your system/network/etc…

What are blocks?

Blocks are the most important component of blockchain technology. In a block, you can store any type of information that you want. Each block contains a set of transactions and is linked to the previous block, creating a chain. Blocks are created by miners and verified by consensus mechanisms in order to be added to the chain.

A block can contain any type of information: transactions, contracts, smart contracts (which we’ll get into later), digital assets like cryptocurrencies or tokens–anything at all!

What’s the difference between a full node and a light node?

Full nodes are computers that store the entire blockchain, which is a database of all transactions in the network. Full nodes verify each transaction using all of this information, which means they’re able to detect double-spends and other fraudulent behavior.

Light nodes, on the other hand, store only part of this data–usually only what’s necessary for them to operate as part of their private blockchain networks (the individual blockchains). Light nodes use full nodes as trusted third parties when verifying transactions on behalf of other users in their own blockchains; if you’re using one as part of your company’s private chain but don’t want to be responsible for storing all that information yourself or verifying all those transactions yourself every time someone sends money through your system then light node technology could help save space while still providing enough security for most purposes.

How do you update blockchain technology?

There are two ways to update blockchain technology: a hard fork or a soft fork. A hard fork is when the software of an entire blockchain gets updated and everyone on that chain needs to upgrade their software in order for their transactions to be valid. This can be difficult, as it means you need everyone’s cooperation in order for your transactions to go through. If not enough people upgrade their software with you, then what? Do your transactions still go through? Who knows!

A soft fork is when only part of the network has been updated with new rules while another part hasn’t been updated yet–which means there will still be some nodes running old code while others run new code (and vice versa). But because there are no rules saying which version should win out over another in terms of validity when two chains exist side-by-side like this, eventually one side or another will become dominant by virtue of being able-bodied enough to keep processing payments as normal even if some other parts aren’t cooperating yet.”

A blockchain is an open, distributed ledger that can record transactions between two parties efficiently and in a verifiable and permanent way.

A blockchain is a digital ledger that records transactions between two parties efficiently and in a verifiable and permanent way. This open, distributed ledger can be shared among many participants in the network and it allows them to verify each other’s data by consensus.

A blockchain consists of blocks that hold batches of valid transactions (or contracts). Each block contains:

- A hash pointer to the previous block; this links them together into a chain so that if you change one block, all subsequent blocks will need to be updated as well (this is what makes them immutable).

- A timestamp for when it was created; every new transaction must contain data about its creation time so it can be verified against previous entries on the chain before being approved by miners who verify all transactions before adding them onto their own copy of this record via mining algorithms using their computing power instead of relying solely on trust in central authorities like banks do today

Conclusion

We hope this article has helped you understand the basics of blockchain technology. As we mentioned before, it’s a very complex topic that can take years to master–and even then! But if you want to get started with your own project or just learn more about what makes this technology so special, there are plenty of resources out there for you.