Introduction

Blockchain is a digital ledger of transactions. It’s the technology that underlies cryptocurrencies like Bitcoin, Ethereum and Litecoin. The system was created to make it possible for people to transfer money without relying on banks or other financial intermediaries, but it can also be used in many other ways:

What is blockchain?

Blockchain is a distributed ledger, or database, that maintains a continuously growing list of data records. These records are called blocks and they’re linked together through cryptography to create an immutable chain.

The blockchain network consists of computers (called nodes) which are connected to each other via the internet. Each node stores an identical copy of the ledger and processes transactions in order to reach consensus about what transactions should be considered valid or invalid by other nodes on the network. This allows them all collectively verify if any given transaction is valid without having to trust anyone else because everyone has access to exactly same information as everyone else at all times – there’s no central server being controlled by some company or government agency where someone could tamper with things undetected!

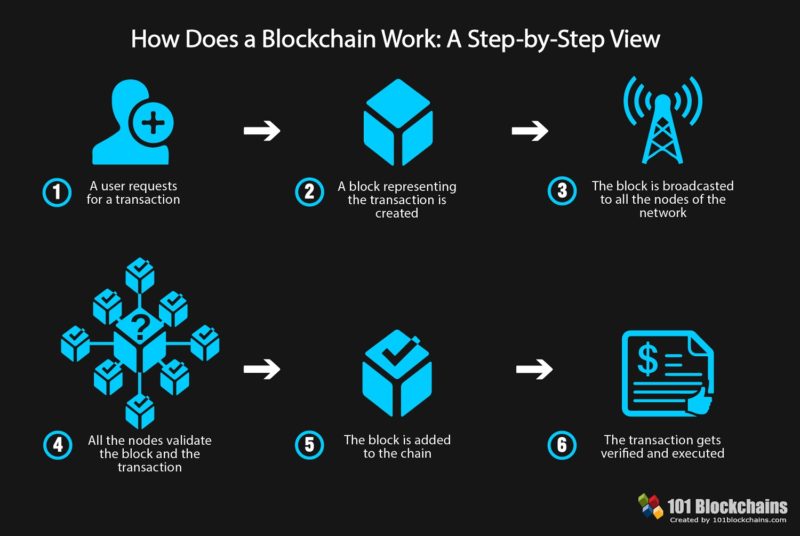

How does it work?

- Blockchain is a decentralized ledger.

- Blocks are added to the ledger by a network of computers.

- Each block contains a cryptographic hash of the previous block and transaction data.

- Blocks are linked together to form the blockchain, which records information about every transaction ever made on its network in chronological order from top to bottom (hence “blockchain”). The blockchain is stored on each computer in the network, making it virtually impossible to tamper with or alter any record without every node noticing it immediately and rejecting your changes as invalid.*

What are the limitations of traditional banking systems?

Blockchain is a new technology that has the potential to change the world. It’s an open-source, decentralized ledger for recording transactions across many computers. But what does this mean for you?

A traditional bank or credit union may have one centralized database with all your information in it–your name, address, phone number and account balance. If someone got access to that database and changed any of your information (like making yourself seem wealthier than you are), then everyone who uses their service would be impacted by that change because they’re all using one central system with no way of verifying if something has been altered or not. With blockchain technology however; each user holds onto their own private key which allows them exclusive access over their own data while still being able to interact with other users securely via public ledgers like Ethereum & Bitcoin where anyone can view but only those who hold keys will be able to update information stored within these chains without needing permission from others first!

How can blockchain help with data protection and security?

Blockchain is a decentralized database that uses cryptography to ensure that data can be accessed only by those who have permission to do so, as well as ensuring that the data has not been tampered with in any way.

Blockchain technology makes use of several concepts:

- A distributed network of computers (nodes)

- Encryption to secure information from unauthorized access

- Timestamping and hashing (and other methods) to ensure that no one can alter records once they are added

Can it fix issues with data privacy, fraud and identity theft?

Blockchain can help with data privacy, fraud and identity theft. It’s decentralized, immutable and transparent.

What are the benefits of blockchain for business and government organizations?

Blockchain is a powerful tool that can be used to improve business and government organizations in a variety of ways. Some of the most beneficial include:

- Cost savings – Blockchain technology reduces costs associated with processing transactions by eliminating third parties, who are often needed to ensure that both parties are satisfied with their agreements. For example, if you want to send money from one country to another, there will be fees associated with each step along the way–from banks or other financial institutions acting as intermediaries between sender and recipient or even at different locations within those institutions themselves (such as headquarters vs branch offices). By using blockchain instead of traditional methods for transferring funds across borders or within countries where multiple currencies might be involved (e.g., USD vs EUR), companies can save money on these fees while also improving transparency in how much it costs them overall.* Decreased transaction times – Since no outside party needs verification before completing each transaction on top of having access immediately after being recorded onto blocks containing all previous transactions made through various blockchains around world time zones simultaneously rather than sequentially like traditional databases do; this makes them faster than traditional systems which usually require some kind of manual intervention first before any type action taken place.* Increased transparency – Both consumers/customers AND businesses benefit greatly because they know exactly what’s going on behind closed doors regardless whether good news bad news since everything written down somewhere else besides just memory alone

Blockchain technology offers a way to store, manage and transfer ownership of digital assets in a decentralized manner.

Blockchain technology offers a way to store, manage and transfer ownership of digital assets in a decentralized manner. The blockchain is a digital ledger of transactions, which can be programmed to record not just financial transactions but virtually everything of value. The blockchain is a public ledger that records all transactions across many computers at the same time.

Conclusion

Blockchain is a new technology with the potential to transform many industries, but there are still some challenges for it to overcome before it becomes mainstream. These include scalability issues that need to be addressed as well as regulatory concerns about data privacy and security in such a decentralized system. However, if these issues can be resolved then blockchain could transform how we do business today by improving efficiency across all sectors while reducing costs thanks to its distributed ledger system which improves transparency at every level of operation.”